Which Self-Directed Retirement Plan is Best for Me? Part II [CHECKLIST]

*This blog post is the second and final article in our two part series. You can read the first article here.

*This blog post is the second and final article in our two part series. You can read the first article here.

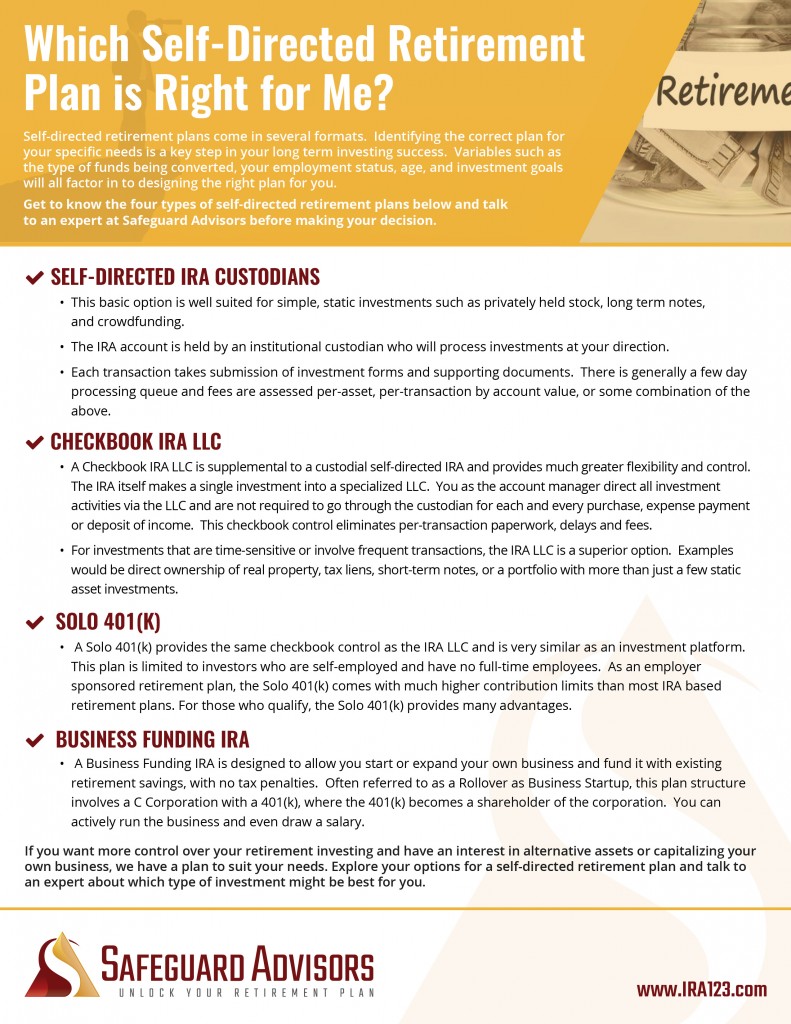

Our first article of the series “Which Self-Directed Retirement Plan is Best for Me” addressed overviews of two plans, self-directed IRA custodian and checkbook IRA LLC, to provide insight about the types of available plans. This is the second and final article in the two part series that will focus on the solo 401(k) and business funding IRA retirement plans.

Solo 401(k)

A Solo 401(k) is similar in many respects to the IRA LLC. You as the investor will operate out of a bank/brokerage account of your choosing and will have signing authority. The key difference is the back end retirement plan and how it functions.

A 401(k) is an employer sponsored retirement plan. A business establishes a 401(k) as an employee benefit. The Solo 401(k) is a simplified implementation designed for owner-only businesses. Because there are no non-owner employees participating in the plan, the plan administration is greatly simplified.

As a qualified employer plan, a 401(k) has much more generous contribution limits than most IRA plans. While a traditional or Roth IRA is capped at $6,000/$7,000 depending on whether one is under 50 years old or 50 and above, a Solo 401(k) can accept contributions up to $57,000/$63,500.

Unlike IRA’s, 401(k) plans offer a participant loan feature, meaning that you can borrow from the plan on a limited basis. This can be handy for starting a personal business.

On the investing side, the 401(k) has an advantage for those investors looking to use leverage such as a mortgage when purchasing plan assets. An IRA is subject to taxation known as UDFI on the portion of income derived from debt financing. A 401(k) is exempt from this tax.

A 401(k) is a specialized form of trust, and you as the self-employed business owner serve as the trustee. As such, you have direct control over the plan funds, without the need to establish a self-directed IRA custodial account or form a LLC. In states with high LLC fees, this can be a significant cost savings each year.

If you and your spouse are both employed by your business, you can both participate in the Solo 401(k) plan.

While tax deferred retirement savings such as a Traditional, SEP or SIMPLE IRA, or an old 401(k) can be rolled over into a new Solo 401(k), there is no ability to accept existing Roth IRA funds. The Solo 401(k) does, however, have the ability to accept new contributions with Roth tax treatment, and you can convert traditional funds rolled into the plan to Roth status.

Not everyone can take advantage of all these great features of the Solo 401(k) however. This plan is only available to self-employed participants with no full time employees working more than 1,000 hours per year. Even if you have such a business, if you or your spouse have a separate business with employees, you may not be eligible for the 401(k). If you are self-employed, but nearing full retirement, the Solo 401(k) might not be the best choice, as it will have to be shut down when the business activity ceases.

Business Funding IRA

The Business Funding IRA is an entirely different format from the 3 plan types covered previously. While those plans are designed for arm’s length investments and provide tax sheltering for the income from such investments, the business funding IRA is designed to allow you to function as an owner-operator of your own business and draw a salary.

The plan itself is not actually an IRA, though it can be funded from an existing IRA or 401(k) account. The business funding platform is comprised of a subchapter C corporation in which the company profit sharing plan can make an employee stock option purchase (ESOP). Basically, your retirement plan becomes a shareholder of the corporation, and the capital can be treated like any other shareholder capital for purposes such as starting or acquiring the business, purchasing inventory, advertising, employee salaries, etc.

While there are no taxes or penalties associated with transferring an existing retirement plan into this format, the business itself will operate in the taxable realm.

For those individuals wanting to pursue the dream of owning their own business, this can be a great opportunity.

This plan is not designed for engaging in passive investments such as rental real estate. The business must be an active endeavor providing a service or product, for example.

Because of the cost and complexity of this program, a minimum investment of $100,000 is recommended.

Summary

A self-directed IRA, checkbook IRA or solo 401(k) program can be a great way to diversify your retirement portfolio into non-traditional assets such as real estate. Finding the right plan for you depends on your situation and goals. Be sure you consult with experts to determine the best solution for your needs. For those individuals looking to own and operate their own business, and fund that business with existing retirement savings, the Business Funding IRA presents a great opportunity suited for this unique purpose.

NOTE: Contribution limits on this page are current as of the 2020 tax year.

Download our checklist below to learn more about these self-directed retirement plans,

and determine which one is right for you.

Talk to An Expert Today!

Learn these little known strategies and tactics, and unlock your retirement plan today.

{kind=link}